Return the Dividend!

Terminal Value Mismatch

It is an insane concept that a company can traverse the entire corporate lifecycle, from birth to death, and never return a single dollar to shareholders.

No, buybacks don’t count. Buybacks effect the “permanent” shareholder in the same way that paying down debt does. Both act as a promise of a larger claim to future operating cash flows. But what if that future never comes?

Terminal value is not just a duration concept. It is subject to default risk as well. Not every company will live forever, yet we value them as such…

The mechanics of buybacks are simple. Consider the “permanent” investor - the guy that will stick by the company through thick and thin. The corporation uses proceeds from the business to buy out the surrounding shareholders - these can be traders or retirees or whoever. In doing so, the share count decreases and raises the ownership stake for the “permanent” investor. But he hasn’t actually received any cash yet. Just a higher ownership stake in the future prospects of the business.

The business can, in theory, do this forever. If a company has a 10% earnings yield, they can decrease the share count by 10%. And they can do that year after year. And every year, the earnings per share will rise by 10% and the stock price should rise along with it.

But what if the future prospects of the business become impaired? AI, overnight, became an existential threat to software stocks like Adobe. And even though revenues and earnings haven’t yet shown impairment, it’s still possible that their days are numbered. At least, that would be the implication one would gather by inspecting current price-action.

I have no real opinion, either way…at least not one that would add any meaningful insight to the conversation. But it does raise some interesting questions about the way we value companies.

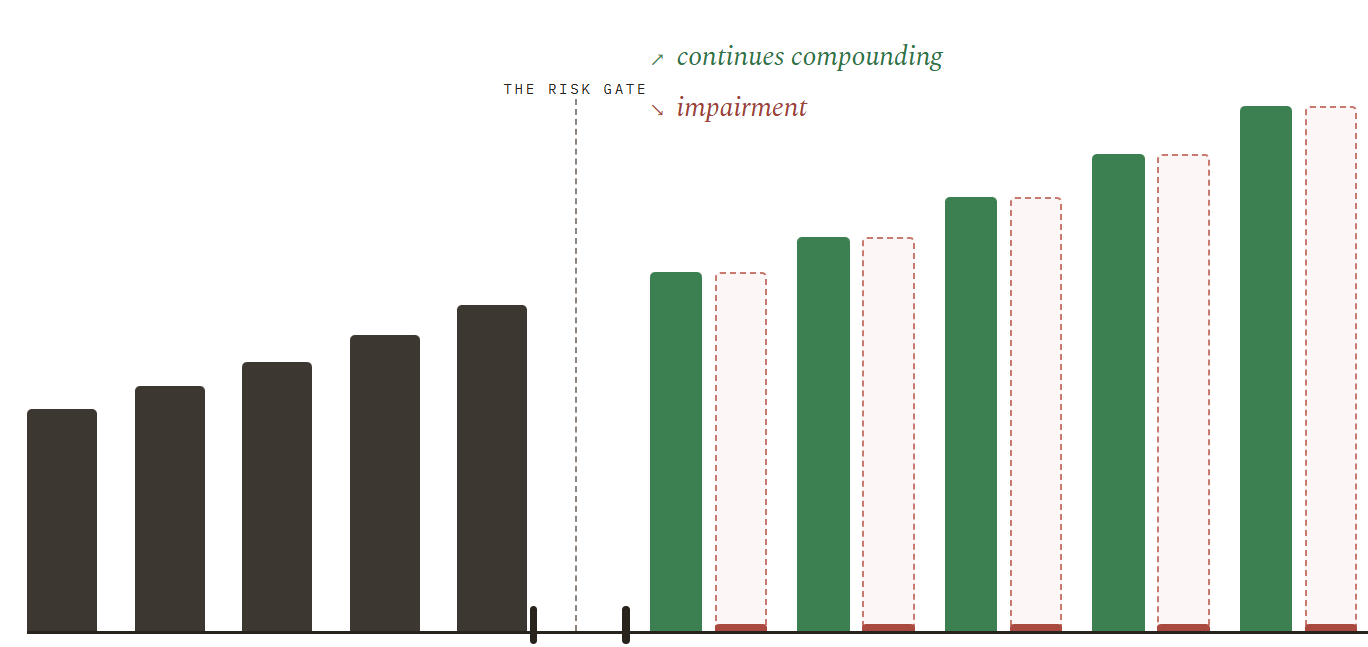

Let’s say that a company faces an existential threat a handful of years from now. They have a buyback-only policy and buyback shares all the way into judgement day. Next year’s earnings are expected to be $10 per share, and that will grow 10% per year strictly due to buybacks (underlying total net income does not grow). If they survive the risk gate, they continue buying back shares as usual. In this scenario, let’s say the stock is worth $100.

If the company doesn’t survive the risk gate, the stock is worth zero.

The next natural step would be to perform an expected value calculation on this scenario. If the path probabilities were 50-50, the stock would be worth $50. This would be the fair value of the company’s stock today.

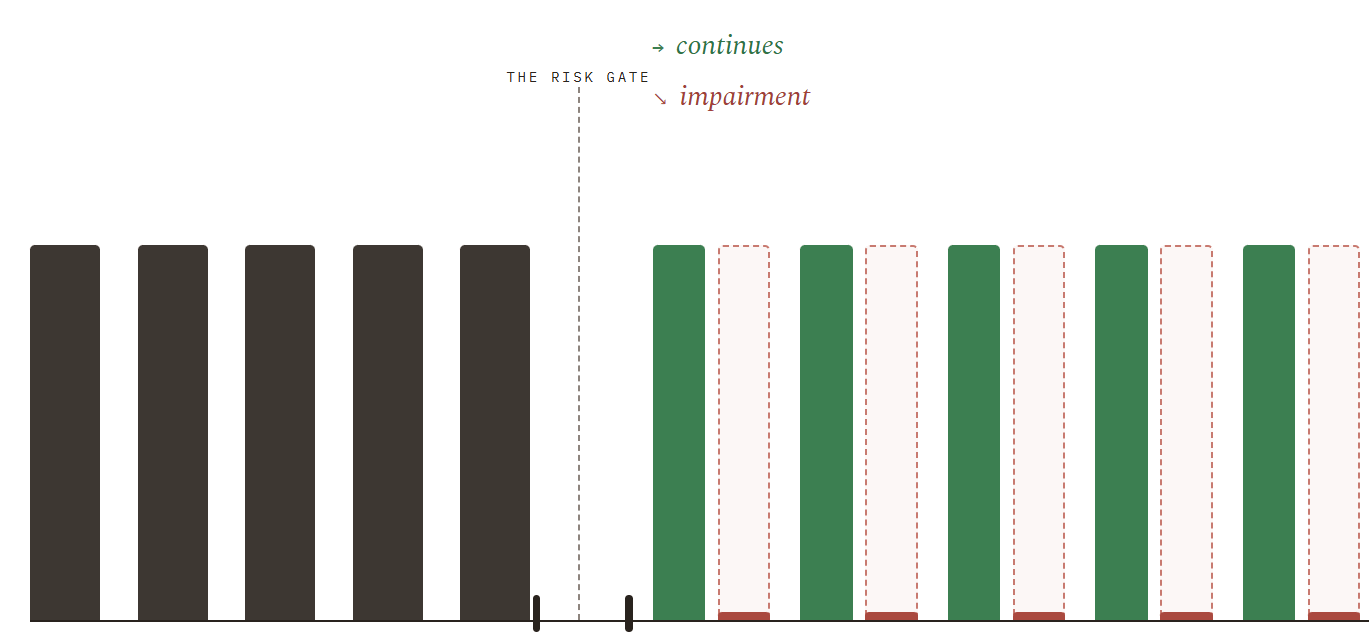

Now, let’s consider an alternative scenario where instead of performing buybacks, the company simply issues a $10 dividend every year.

Note that since the underlying share count isn’t changing, there’s no compounding of the earnings / dividend.

The stock is still worth the same $100 in the event of surviving the risk gate (green).

The impairment scenario changes a bit, however. The stock is worth $0 after the impairment event. But this time, investors received $50 worth of dividends before impairment. These dividends have a present value of about about $38.

Running the expected value exercise, now, gives a fair value of $69(nice) per share.

The dividend scenario is worth nearly 40% more ($69 vs $50). This is simply a function of managing risk and duration.

When we look at today’s stocks that are currently being taken to the woodshed despite seemingly strong underlying fundamentals - Paypal, Adobe, Charter Communication, etc - it’s due to investors applying more weight to the impairment scenario (red bars).

Managements of these companies could easily lift the value of their share prices by instituting a dividend policy.

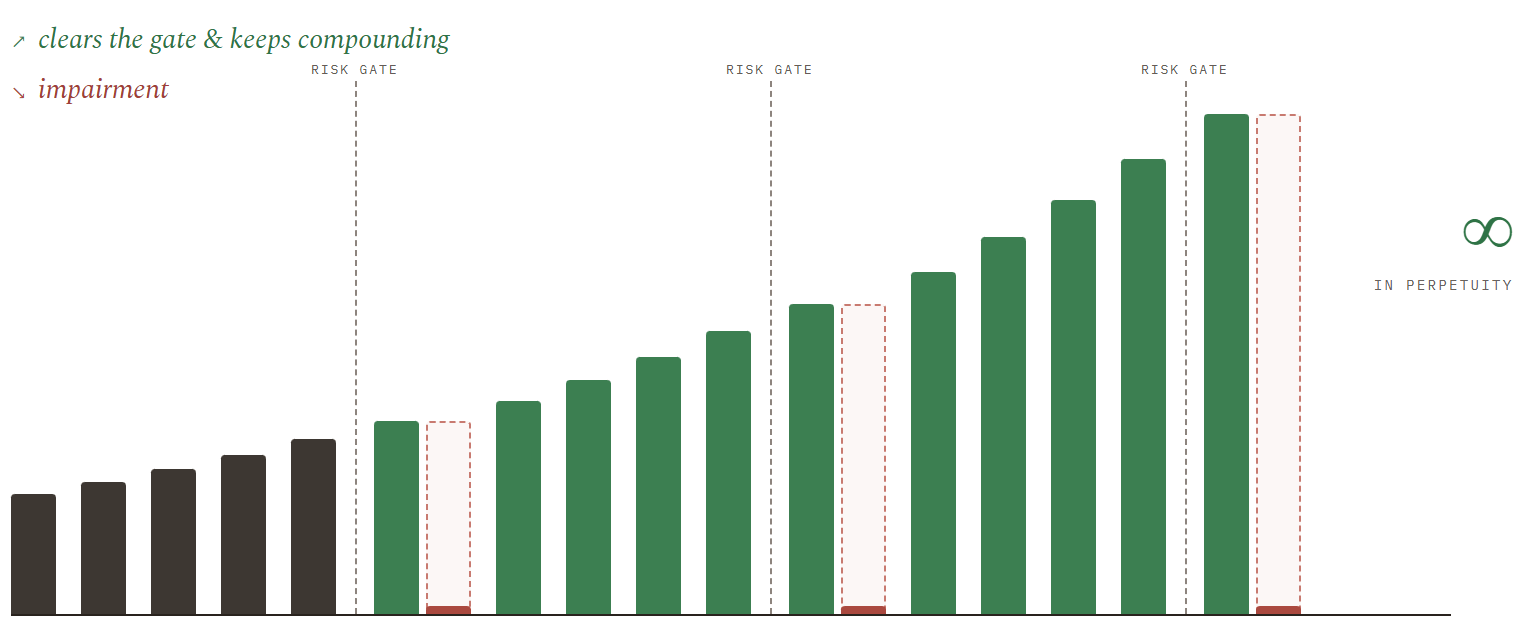

There’s another interesting artifact of this type of analysis.

Impairment threats are ever present. They exist in the form of innovation disruption or economic recessions & credit cycles, etc.

If we knew, today, that a company was never-ever going to pay a dividend, the resulting value would be zero because it’s a certainty that eventually they won’t survive a risk gate.

This dynamic is not too dissimilar to “letting it ride” at a craps table. Given enough time, busting is a certainty.

Buybacks are a terrific concept. But they are predicated on the assumption that the company will live forever. When risks pop up, whether perceived or actual, the buyback policy can actually be detrimental to the share price.

We give a lot of grief to private credit Payment in Kind (PIK) structures. But share buybacks are effectively the same concept. At some point, you actually have to return cash to your investors.