Shareholder Yield

How Debt Factors into the Equation

…when facing difficulty achieving high rates of return on their capital, companies can return cash to shareholders via cash dividends, debt paydown, or stock buybacks.

~ Meb Faber,

Most investors understand that dividends and share repurchases are the bread and butter of shareholder yield. Far fewer include debt paydown into the equation. And even fewer, still, incorporate it correctly - not even Meb Faber.

Today, I want to explore why debt paydown is a critical component of shareholder yield, and how we should go about incorporating it.

Debt Paydown Effect

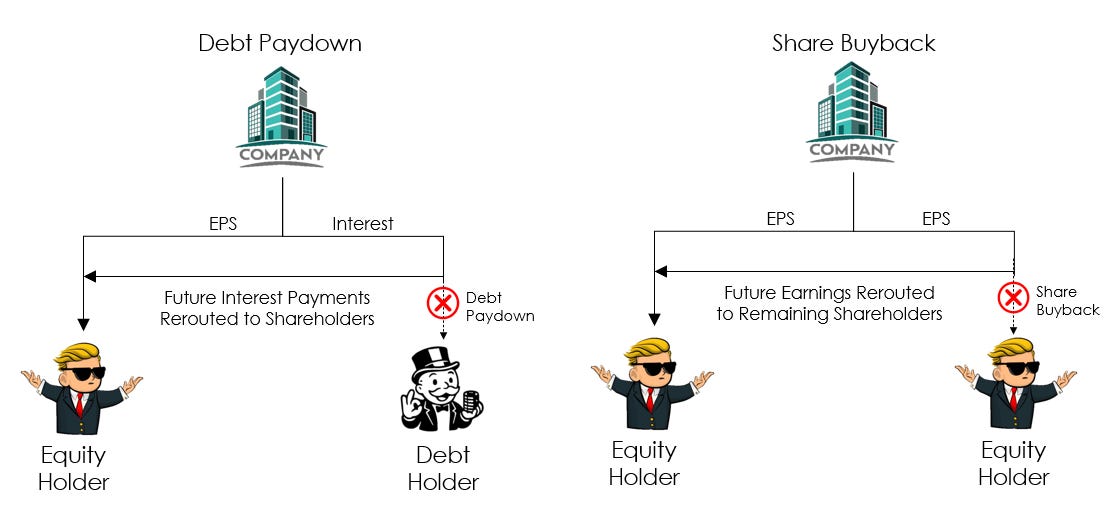

To think about why we’d include debt paydown as part of shareholder yield, we can look directly to share buybacks as a corollary.

In the case of buybacks, there’s no actual return of capital to shareholders that choose to continue holding their stock in the same way that there’s no direct return of capital to shareholders when debt is payed down.

However. They both share the same mechanics in that future cash flows that belonged to the original stakeholders are now redirected to the remaining stakeholders.

Debt Paydown & Shareholder Yield

There’s a common mantra that companies should only do share buybacks when the stock is undervalued. The reason for this is simple - if investors shouldn’t overpay for a companies stock, neither should it’s management.

What this means, in real terms, is that share buybacks that are performed above intrinsic value have a diminishing impact on shareholder yield. The same is true for debt paydown. Because cost of debt and cost of equity aren’t the same, the rerouting of interest payments will have a diminished effect on the value of future earnings to shareholders.

Let’s do a quick example:

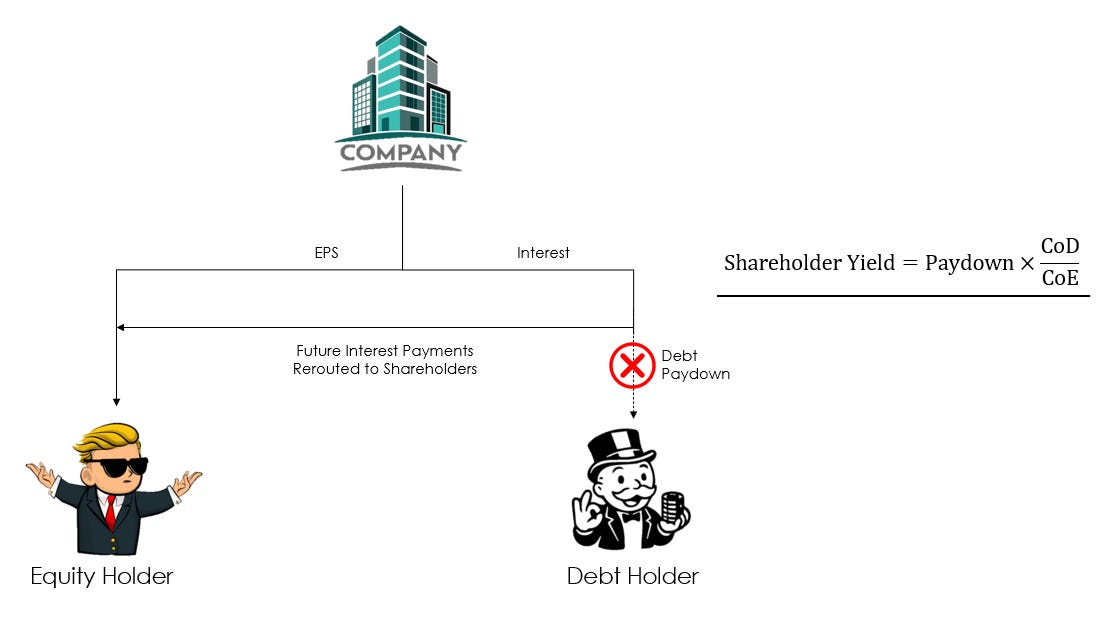

Consider a company that has $500 million in debt at 1% interest - $5 million per year in interest payments going to debt holders. Now let’s say that the company decides to retire that debt when it reaches maturity.

The proper way to price that event is to assume that the $5 million per year in interest payments gets rerouted to shareholders. At a cost of equity of (say) 8%, the new-found stream of cash flows is worth $62.5 million to equity holders ( $5M / 0.08 ) - much less than the $500 million that was paid down. To apply this paydown effect to shareholder yield, you’d divide $62.5 million (not the full $500 million) by the market cap of the company. So we see that shareholder yield doesn’t perfectly scale with debt paydown.

This same relationship holds for share repurchases, only the discount rate in the numerator would be the cost of equity; which is the reason why shareholder yield scales 1-to-1 with the share repurchase amount. There’s an important caveat that this assumes that shares are repurchased at fair value. One can run through the exercise of showing why shareholder yield is disadvantageous when the stock is trading above fair value and vice versa when trading below fair value. I won’t do that here.

There’s an additional caveat that this assumes that these diverted cash flows last forever. After all, recurring cash flow divided by cost of equity is just a terminal value calculation. So one needs to take special care to verify that the company in question has a long life expectancy. If you find a business that is aggressively buying back stock or paying down debt, but their revenue is deteriorating...run

Debt & Equity Pricing Interaction

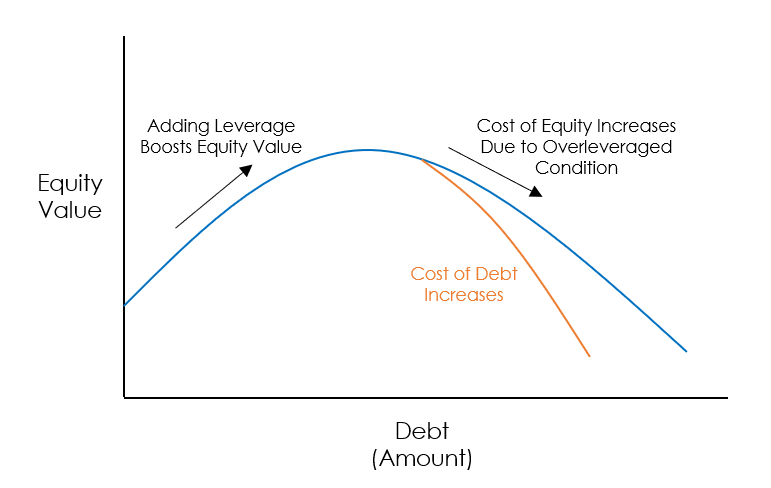

Let’s start with a simple thought exercise. Consider a company that starts with no debt. What happens to existing equity holders when that company adds their first marginal dollar of debt to the balance sheet?

The simplest example would be issuing debt and then turning around and immediately paying the full amount to shareholders as a dividend. That results in a higher return to the equity holder - we’re trading cheap capital (debt) for expensive capital (equity).

But corporate leverage is also already well known to boost equity returns. A real estate property might have a cap rate of 4%, but when combined with debt, it can yield investors double digit returns. This relationship is largely well understood.

More broadly, management can tinker with the capital structure of the business, and improve the value of the equity holder’s stake by adding cheap debt to the balance sheet.

This is the “bull case” for having some debt.

The Next-Dollar of Debt

From there, how do we think about how the next marginal dollar of added debt to the balance sheet? Obviously going from $1 of debt to $2 doesn’t really change much. But, what happens as we start to approach higher and higher debt to equity or interest coverage levels? At some point, the business, at large, becomes more fragile.

What we see is that the first dollar of debt improves the value of equity, but we eventually reach a point where the rising risks to equity overtake the provided benefits of leverage. Beyond that point, the marginal dollar of debt actually begins to hurt equity values.

In addition, as more debt is piled on, the company’s credit rating likely deteriorates, and results in the cost of debt going up which further exacerbates the situation (orange).

Debt Paydown on Shareholder Yield

So what does all of this tell us?

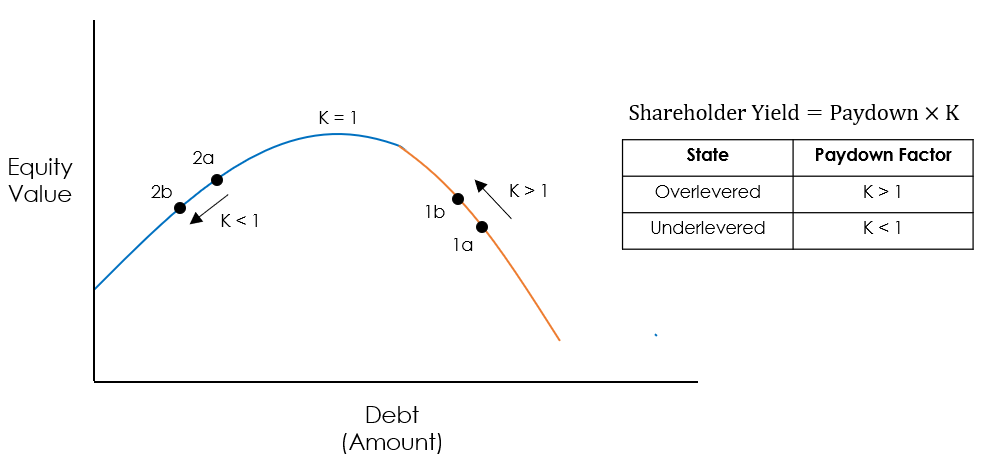

We know that when a company is in good financial shape, the debt paydown effect on shareholder yield is very much diminished. The true shareholder yield will be decreased to somewhere in the range of the ratio of CoD / CoE.

Conversely for a company that has gotten too hopped up on debt, paydown of said debt actually improves that risk profile of the business as a whole, and can actually result in a multiplier effect to the debt component of shareholder yield. As in the case of points 1a to 1b. This would typically manifest in the PE ratio increasing as the business de-levers1.

A Note to Management

One company that I think would benefit from reading this article is Verizon. They have $175 billion in debt and a debt to equity ratio of 1.65. They also have roughly $20 billion in annual free cash flow, but send most of it out as dividends. If, however, they suspended the dividend and focused on paying down debt, equity holders might actually experience better returns.

First, consider what the PE ratio for a hyper-stable business like VZ should be if they weren’t saddled with so much debt. I don’t think it would be unreasonable to assume that their potential PE ratio would be somewhere in the mid 20x range if they brought down their D/E to 0.5 (for instance). It would take 6 years to get there if they dedicated the full annual cash flow ($20 billion) to that effort. In this instance, multiple expansion from 8x to 25x in six years would yield 21% annualized returns…much better than their current 6% dividend + anemic price performance.

I’m just making these numbers up, and maybe there’s some structural reason why VZ shouldn’t trade at a higher PE ratio, but I think the overall point still makes a lot of sense.

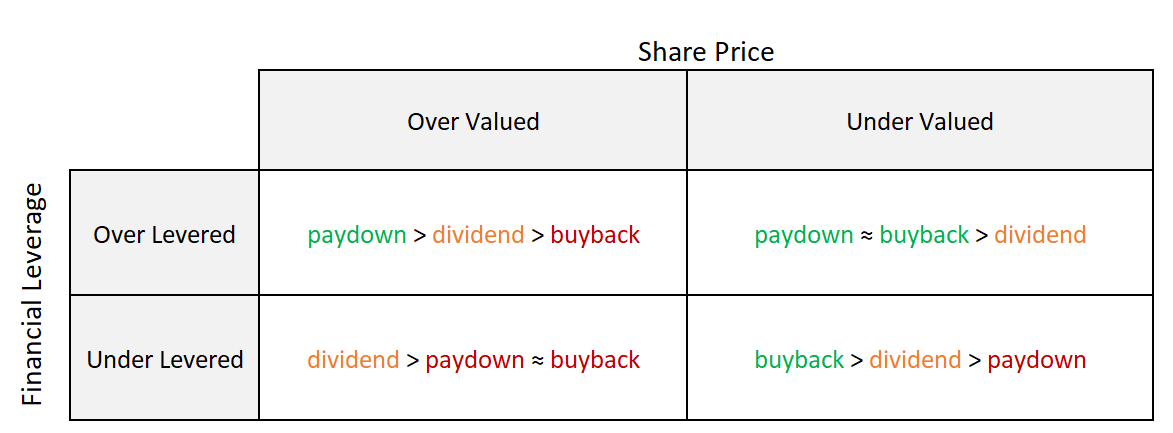

More broadly, here’s a decision matrix for companies that want to think about how to distribute their cash flows:

Shareholder Yield Summary

This general calculation for shareholder yield is as follows:

Note that I never made an attempt to explicitly define “K” - the knockdown factor. That’s on purpose. There are methods for finding these impacts: Modigliani-Miller Proposition II is one of them. But I think it’s more useful to know how to think about the interaction between debt and cost of equity, qualitatively.

For a low levered company, K will simply be the (cost of debt)÷(cost of equity)

For companies where the analyst believes the level of debt on the balance sheet puts equity holders at risk, then it makes sense to use a value of K ≥ 1.

One takeaway from this exercise, is that investors might actually want to screen for highly levered companies. Combined with a high shareholder yield and an aggressive commitment to pay down debt, these companies could offer the opportunity to capture decent excess returns.

Note that I realize I’m somewhat conflating two different mechanisms: cashflow redistribution & risk components. At the very least, this is a useful heuristic.

Thanks a lot, I really enjoyed reading this very well written article on capital returns. I love the Verizon example and how you argue that they and their shareholder could materially benefit from a reduction in debt. I recently looked for the reason why Verizon does not pay down it's debt (there is a comfortable free cash flow). My conclusion is that VZ lacks lucrative investment and growth opportunities that would take valuation to a different level. They sit comfortably on their stable cash flow and return it to shareholders as dividend or coupons. If they didn't I believe there would be little incentive in the market to buy this stock.